Recognise Your Tipping Point and Take Action before it’s Too Late!

Read on for our 5 Action Strategies!

Tipping Point, Breaking Point or Boiling Point, terms most likely you have heard. Described by Cambridge Business English Dictionary as, ‘a time during an activity or process when an important decision has to be made or when a situation changes completely’.

This Tipping Point once reached can be the difference between success or failure. To go forward or stop! There is a reaction. One that takes you onto bigger or better things or is the opposite, the equilibrium unbalance causing you, the scales to topple over into a downslide or stagnation.

For Small Business: What does it Mean in Reality?

If you are a Small Business struggling with the current inflationary pressures you may be reaching your tipping point. For example, how to respond to spiraling costs of supplies, wages and overheads. At what point do you tip over the edge. Customers are becoming thriftier and more selective in their shopping habits, while still chasing value and quality.

In seeking solutions do you increase your prices and at what point will you tip the balance and lose customers. Alternatively, keep absorbing the costs, reducing and losing your profitability until closure.

Example:

Cafe 1, cup coffee $6 increases to $8 a 33% increase.

Cafe 2, same cup $6 increases to $6.50 (16% increase), with gradual increases over two rises. i.e.incremental increases to reach the tipping point.

Alternatively, a lump sum increase can the tip point and lose customers.

What is your breaking point?

What to do!

Take action by understanding what a Tipping Point is and how to identify it.

A Tipping point is the turning point at which a product, brand, or company becomes either highly successful or faces failure. The ‘scales’ will topple or tip over to positively or negatively! With the latter, reaching a Tipping point at which damage is irreversible or accelerating.

Better to see and heed the warning signs!

- Profit margins reducing

- Cashflow challenges

- Sales turndown

- Customer complaints

- Supply issues

5 Action Strategies:

- Identify the problem. Gather all relevant information. Avoid putting it off.

- Bring your Team together. Put the issue on the ‘table’ to brainstorm problems and seek solutions.

- Reach out to your Customers. Be upfront, connecting with honest and open communication. Don't apologise.

- Engage a Business professional advisor if needed.

- Speak with Blackburn Accounting let us help you get on top of your Business matters

Read more...

7 Strategies and Tips to help You and your Business Achieve Success!

7 Strategies and Tips to help You and your Business Achieve Success!

What does it take?

Ask a successful small Business owner and no matter the decade or era, sentiments expressed include; hard-work, commitment, having a dream, belief, giving good ‘old-fashioned’ customer service, a little good luck, careful financial management and stamina!

And throw in being open to change and the unexpected!

Sounds daunting! But don't give up!

Whether you are starting out or are already established there are sound Business practices and strategies that if adopted provide direction for success.

First, it’s important to define what success means to you, how it looks and means to achieve it. High profits, supporting local communities, going viral, or social impact, whatever the measure or motive there are some common Strategies & Tips to achieving Business success. Here are 7!

-

Have a Clear Vision – identify, know what your Business is. What do you and your Business stand for, what do you want to achieve, deliver. Your purpose, message!

Tip: Be true to your mission, have belief, passion and commitment. Picture Blue Sky but avoid having your head in the clouds!

-

Develop a Solid Business Plan - This is crucial, as the foundation of your Business and your guide. Create goals, short and long term with KPIs, along with financial projections. Monitor and measure progress.

Tip: Reassess your goals and adjust if needed. Scrutiny of KPIs is imperative to identify results and underperformance.

-

Embrace Digital – Technology and Business automation is key to growing your Business. It's staying agile and scalable, from cloud computing to smart Business tools like project management software. There is a range of digital solutions to help small Businesses, by improving efficiencies and cutting unnecessary costs to enhance profit margins.

Tip: Key to leveraging technology solutions is to determine what tech aid can benefit your Business operations.

Read more...On 9 May 2023, as part of the 2023–24 Budget, the Australian Government announced it will improve cash flow and reduce compliance for small businesses by temporarily increasing the instant asset write-off threshold to $20,000, from 1 July 2023 until 30 June 2024.

This measure is not yet law.

Small Businesses, with aggregated turnover of less than $10 million, will be able to immediately deduct the full cost of eligible assets costing less than $20,000 that are first used or installed ready for use between 1 July 2023 and 30 June 2024.

The $20,000 threshold will apply on a per asset basis, so small businesses can instantly write off multiple assets.

Assets valued at $20,000 or more (which cannot be immediately deducted) can continue to be placed into the small business simplified depreciation pool and depreciated at 15% in the first income year and 30% each income year after that.

Read more...

Family run Businesses the backbone of Australia’s economy.

What does it take to keep this essential lifeforce operating!

A question many Businesses face, ponder and deliberate over! You might be one of them!

What are the do’s and don’ts to running a successful family Business and having a happy family!

Here are 8 Tips!

- Open Communication and Respect

- Treat Your Business Like a Business

- Effective Structuring

- Cashflow – Keep on top of it!

- Document Everything

Success is a personal experience that can mean and look different for everyone depending on their values and goals.

Cambridge dictionary defines; ‘The achieving of the results wanted or hoped for’. Or expressed as; ‘True success means staying true to a deeper sense of purpose, despite deviating from a superficial social norm. It means having the courage to peruse one's own journey when confronted by the fear of uncertainty.’

What are your thoughts! How do you define success!

Do you relate to these components?

- Feeling of accomplishment

- Financial stability

- Personal fulfilment

- Social recognition

- Professional achievement

- Making a positive difference

- Enjoying your work

- Treating others with respect

To reiterate, ‘Success – What Does it Mean and Look like to You!’

Have you achieved what you want, fame, fortune! Yes, congratulations!

Or are you still searching, wishing and hoping. If that’s you, don’t delay, understand what success looks and feels like for you and take the necessary steps to achieve it.

Here are 7 Tips for defining success and setting goals:

- Reflect on your values: Consider your values and how they align with your personal and professional aspirations.

Success can be different for everyone, fame, fortune, happiness! All of those and more!

How you define it will vary as will the factors shaping it. It can look, feel and be different for us all!

If you are a Business owner it also depends on your lifestyle, goals and aspirations and what you hope to achieve with your small Business, now and long term.

When you consider all these factors and influences, and which are the most important, you might see Success as providing benefits.

The 6 Benefits of Success

- Improve Cashflow

- Reduce risk

- Have clear direction

- Take action

- Develop a winning Team

- Having fun

Success looks like, feels like:

- achieving specific measurable goals and objectives,

- overall satisfaction, belief in self and Team

- being emotionally and financially stable, peace of mind

- doing what you love and enjoying your work everyday

- reward with profit for hard work

- making a difference, with personal effort, quality products and service.

Let's look more closely at the 6 Benefits of Business Success:

1. Improve cashflow:

A regular and smooth flow of money in and out of the Business necessary for daily operations, and costs including paying employee's, purchasing stock, and taxes. Positive cashflow indicate the Business liquidity.

There are 9 Ways to Help get your Cash flowing. Click on link.....https://blackburnaccounting.com.au/blog

2. Reduce Risk: Risk comes in different ways requiring different strategies to manage.

Read more...

In these challenging economic times, it’s tough going for many, small Businesses and households alike are experiencing it. Budgets are stretched to the limit!

If you are a small Business operator it’s very likely you are facing increased pressure to maintain profitability and sales and attract product growth. Not an easy task!

The key is what to do to survive these difficult times.

And there are those, you may be one of them, Businesses that are making it work.

It’s been said before, ‘successful people find a way through tough times’!

But more importantly the question is, 'how do they do it'!

Google ‘successful businesspeople’ and the word ‘entrepreneur’ appears, and with that certain characteristics and traits to describe them. Many enjoy huge success, and they are to be applauded for what they have achieved.

If you are a small Business operator you will probably recognise yourself with the same traits and qualities. You too are to be applauded. You may be one of the everyday small Business owners enjoying the success of running a healthy Business that supports you, a family and Team.

Traits of successful Business people include

- Effective Communication skills:- open, active listening, seek and take feedback

- Adaptability & flexibility: in thinking and actions, embrace change and challenges as opportunity

- Initiates ideas and action orientated to achieve outcomes

- Positive mindset: optimistic, self-confidence & motivation – belief in self, others and take action

- Strong leadership – leads by example, rolls up sleeves, make the hard decisions

Finding a Way through! Here are 8 Ways to consider

Read more...

There comes a time in most Family Businesses when it’s time for the ‘founding’ members to let go, step aside and hand over the reins or baton!

Letting go is a subject of conversation, raised often, particularly when there are problems with the 'changing of the guard'!

This situation, handing over the reins, despite good intentions, often becomes complex and complicated when the ‘founder’ holds on too tightly or for too long. Simply said, they have trouble letting go!

This raises the question ‘why is that so?’

Loss of Identity: Erosion of identity, rather than management, is often the root cause. Stepping away can be a huge change for the owner who has often given their life to building the company. It has been their primary purpose. Succession can feel more like an existential crisis rather than a professional milestone. These feelings should be considered and taken seriously. Seek professional health guidance if needed.

No post-retirement plan: Yes, there has been talk of taking it easy, going on a cruise or catching up with old friends, but without meaningful activities and engagement, founders tend to linger on at the Business. A retirement plan plans for retirement. Being proactive, finding ways, purpose, and making other investments to fill their time.

Read more...

Planning for the future, your future!

Leaving your Business may or may not be in your thoughts right now but at some stage you will decide to leave your Business.

Being prepared for that occasion will make it easier. Whether it is to sell, retire or do something else, having a succession or exit plan in place will help you transition smoothly out of your Business. And who wouldn’t like that!

Succession planning makes sound business sense as it can be the answer or solution to an unexpected event, such as illness or death, helping take the stress and worry out of a difficult time. Early planning can also help to maximise the value of your Business.

For example, there was a large export manufacturing business and the Managing Director, David, was killed from an unexpected motor vehicle accident one morning. The director had no will and no succession plan. The role of Managing Director was allocated to his wife, his next of kin. The wife had never worked in the business and had no relationship with the staff or with customers. The business virtually collapsed without active management. Don't you fall into this situation.

Your Succession Plan must detail the key requirements and any associated legalities.

For example:

- Keeping the Business in the Family

- Buy-sell agreement

- Other options

Keeping the Business in the Family

Read more...Calculate Co-Contributions

Check your eligibility for the co-contribution, it's a good way to boost your super. The amounts differ based on your income and personal super contributions.

If you are able to pay a little extra into your super before the end of the financial year 2024, the government may also make a contribution. Known as a co-contribution, you could receive up to a maximum of $500 contribution from the government into your super account if you are eligible.

Under the co-contribution scheme, the government provides a tax-free superannuation contribution of up to $500, matching 50% of a contributor’s own contributions.

|

Year |

Lower |

Upper |

|

2023-24 |

$43,445 |

$58,445 |

Superannuation What to Know

Superannuation has many facets, what to know, what is required, and what to do. To get the best outcomes speak with a professional about the strategies best suited to your situation.

If you are a Business owner Blackburn Accounting is available to provide professional advice. We offer a broad range of services including personal, Family Business Management, Cashflow Management, Superannuation and retirement planning, and Business Development.

Worth thinking about.

Consider splitting contributions with your spouse if:

- your family has one main income earner with a substantially higher balance or

- if there is an age difference where you can get funds into pension phase earlier or

- if you can improve your eligibility for concession cards or age pension by retaining funds in superannuation in the younger spouse’s name.

- remember any spouse contribution is counted towards your spouse's Non-Concession Contribution cap.

Want to know more, have questions!

Contact us, Blackburn Accounting, we are available and ready to help you with all your taxation and accounting needs.

Read more...

Boost your spouse's super and reduce your tax by making spouse contributions.

Tell me more!

How Does it work?

If you make an after-tax super contribution into your spouse’s super, you may be eligible for a tax offset of up to $540.

Consider this strategy if;

- Your spouse has an assessable income of less than $40,000 p.a.

What are the benefits?

- Grow your spouse's super

- Qualify for a tax offset of up to $540.

How is the spouse offset calculated?

- To qualify for the full offset of $540 in 2023/24 you need to contribute $3,000 or more into your spouse’s super. Your spouse must earn $37,000 p.a. or less.

- A lower tax offset may be available if you contribute less than $3,000 or your spouse earns more than $37,000 p.a. but less than $40,000 p.a.

Example Case study:

Bill and Mary are married and have two young children. Bill works full-time, earning $100,000 a year. Mary has reduced her workload and is now working two days a week and earns $32,000 a year.

The couple want to make sure Mary keeps growing her super while she is working part-time. Bill contributes $3,000 into Mary's super account. This entitles him to a tax offset of $540 which will reduce his income tax when he completes his 2023/24 tax return.

There are important things to consider when exploring the above and eligibility conditions apply. For more information check the ATO website

Need help, have questions and want answers and solutions?

Contact Blackburn Accounting we are your family Business Specialists offering a range of services including Superannuation and Retirement Planning.

Read more...

There is much to know about Superannuation and the following is provided to get you started.

Review your Concessional Contributions (CC) option and new rules:

The Government changed the contribution rates from 1 July 2020 to extend the ability to make contributions from age 65 up to age 67.

Maximise contributions up to CC cap of $27,500 per annum. Be careful not to exceed your limit if your Total Super Balance exceeds $500,000.

It's important to look after your Super!

Need help contact Blackburn Accounting we will answer your queries and sort out any problems.

Checklist for Employers – Superannuation obligations:

As an Employer part of your obligations is to pay Super Guarantee (SG).

Paying your Employees the right amount of Super,have you determined,

- which employees are eligible for super contributions?

- are any contractors eligible for super contributions?

- what payments are considered ordinary time earnings?

- should you apply for a certificate of coverage for employees you are sending overseas?

Have questions, need to know more, if you are a Business owner Blackburn Accounting is available to provide professional advice. We offer a broad range of services including personal, Family Business Management, Cashflow Management and Business Development.

The ATO website also provides information.

Read more...

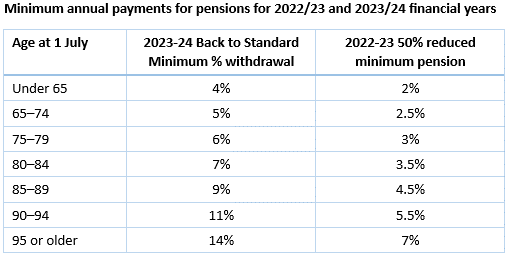

Review Options on Pension Payments

The Government extended the Temporary Reduction in Minimum Pensions as part of the COVID-19 response for FY2023. This program has now finished and the minimum pension payments have reverted back to the normal rates from 1 July 2023.

Superannuation has many facets. To get the best outcomes speak with a professional about the strategies best suited to your situation.

If you are a Business owner Blackburn Accounting is available to provide professional advice. We offer a broad range of services including personal, Family Business Management, Cashflow Management, Superannuation & Retirement planning, and Business Development.

Superannuation updates - Check the ATO website for more information.

Read more... If you have been queuing at the petrol station to get bargain-priced fuel, or indeed to buy any fuel, you will have seen prices increasing dramatically, daily! Welcome to supply and demand economics in play.

If you have been queuing at the petrol station to get bargain-priced fuel, or indeed to buy any fuel, you will have seen prices increasing dramatically, daily! Welcome to supply and demand economics in play.

Or if you have joined the crowds at a for-sale, home open or a property to lease, and left like many without the keys to the front door, you are experiencing the ‘supply and demand’ economic principle. In fact, it is often referred to as the Law of Supply and Demand and is a fundamental concept in Economics.

In simple terms, supply is how much of a product is available in the market, while demand is how much of it people want; together, these form the basic economic theory of supply and demand.

The next part of the equation is the relationship between the two. The amount of a product, commodity or service available and the ‘want’ of buyers to purchase it are the factors determining price.

It's how buyers and sellers interact to determine the price and supply of a resource. When demand outstrips supply, prices will increase. In a free capitalist, competitive market -it‘s economics in play. The price of an entry-level property in Perth now costs twice as much as it did five years ago!

Did you experience these examples? I did! The price of chocolates rose dramatically in 2025, as cocoa production dropped globally due to severe storms. And here we are, April 2026, Easter eggs exemplify the ongoing impact. A leading chocolate maker spokesperson advises, ‘we are navigating higher cocoa and input costs globally’. COVID disrupted and strained global supply chains, transportation and productivity, and subsequently shifted demand patterns. Supply was constrained, and demand spiked.

The same thing occurs with other commodity essentials - toilet paper is a popular item, leaving the shelves like hot cakes!

How it works. Cause and effect! It’s a balancing act!

Read more...Individual income tax rates and threshold changes

On 25 January 2024, the government announced proposed changes to Individual income tax rates and thresholds from 1 July 2024. These changes are not yet law.

From 1 July 2024, the proposed tax cuts will:

- reduce the 19 per cent tax rate to 16 per cent

- reduce the 32.5 per cent tax rate to 30 per cent

- increase the threshold above which the 37 per cent tax rate applies from $120,000 to $135,000

- increase the threshold above which the 45 per cent tax rate applies from $180,000 to $190,000.

For more information see Tax cuts to help with the cost of living | Treasury.gov.au

Read more...

The ATO is warning Business that pay contractors to provide certain services to lodge their taxable payments report (TPAR) for 2023.

The TPAR is used to report the payments made during the financial year to subcontractors or contractors. It is due on 28 August each year.

Be aware, from 22 March 2024, the ATO will apply penalties to those Businesses that haven’t lodged their TPAR from 2023 or previous years or have received three reminder letters about overdue TPAR.

If this is you, act now to avoid paying penalties.

Other – Outstanding Debts

From January 2024, the ATO has an external debt collection agency actioning tax cases they have referred.

This will apply to Taxpayers who haven’t responded to previous ATO contacts attempts or referral warning letters and are not engaged in debt repayment.

Don’t wait, contact the ATO or speak with our team at Blackburn Accounting asap.

Unsure of your responsibilities or what to do?

Need help!

Contact Blackburn Accounting we understand taxation matters,

or contact the ATO directly or check their website for further information.

Read more...

Be prepared!

- If you are a not-for-profit Organisation, be prepared for new reporting requirements to maintain your tax-exempt status.

The ATO has announced this change, which is expected to affect a range of Organisations, from small sporting clubs to major sporting groups, cultural, educational and community and health providers.

- From July 1, not-for-profits claiming exempt status will need to fill out an online questionnaire on the tax office website. The questions are based on the rules for each of the eight categories of exemption.

Need help with understanding these requirements! Contact Blackburn Accounting, we can help you navigate the changes.

Read more...The ATO has registered three data-matching notices on 26 August 2024 for compliance related purposes:

- Notice of a lifestyle assets: The ATO will acquire lifestyle assets data from insurance providers for 2023-24 through to 2025-26 for specified classes of assets, where the relevant asset value is equal to or exceeds the nominated thresholds. The data items include client identification and policy details.

- Notice of a Property management: The ATO will acquire property management data from property management software companies for 2018-19 through to 2025-26. The data items include property owner identification and property transaction details.

- Notice of an Officeholder: The ATO will acquire officeholder data from ASIC, the ORIC, the ACNC, and ABRS for 2023-24 through to 2026-27. The data items include name, contact details, date of birth, ABN, organisation details, state of incorporation, officeholder type, including officeholder role start and end dates.

Read more...

- ATO ramps up warnings on $50b in tax debts.

This warning from the new Tax Commissioner as the ATO chases $50 billion in outstanding debts, claiming increasing numbers of Australian small Businesses operators are falling behind on tax and superannuation obligations.

- At a recent small Business summit in Sydney the Commissioner said ‘it’s critical that all employers, big and small, keep on top of their obligations to their employers first and foremost, as well as their obligation to government in respect to GST, income tax and other taxes’.

- Previously, in November, the ATO warned Business to stop using unpaid tax and superannuation liabilities to prop up their cash flow, stressing its debt book was not a bank.

If these matters concern you, act now, heed the warnings!

Need help? contact Blackburn Accounting, we are experts in taxation matters.

- Tax Debts can affect your credit ratings

Disclosure of Business Tax Debts:

Be aware that in certain circumstance the ATO may disclose your debt information to credit reporting bureaus (also known as credit reporting agencies).

The ATO lists a number of criteria where they may report your Business tax debt. These are provided on the ATO website.

Note: It will not report your debt information to credit reporting bureaus (CRBs) if you are already engaged with them to manage your tax debts and may also decide not to report your tax debt information if you are experiencing exceptional circumstances.

You can find full details on the ATO website.

More from the ATO

Read more... Your Accounting Partner

Your Accounting Partner Your Management Accounting Partner

Your Management Accounting Partner Your Expansion Engineer

Your Expansion Engineer Your Special Projects Partner

Your Special Projects Partner